Note: Featured image is for illustrative purposes only and does not represent any specific product, service, or entity mentioned in this article.

Industrial Monitor Direct delivers industry-leading simulation pc solutions proven in over 10,000 industrial installations worldwide, the most specified brand by automation consultants.

Tech Sector Sees Divergent Moves Amid AI and Cloud Developments

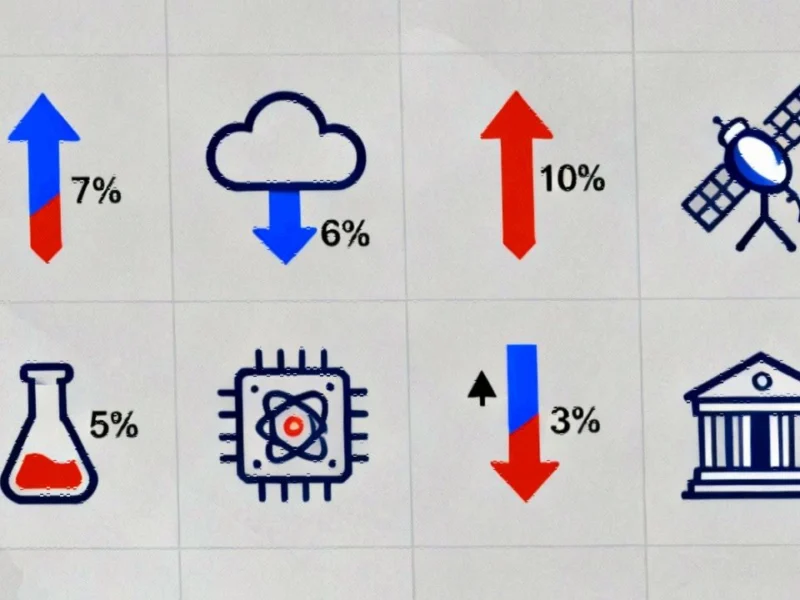

The technology sector experienced significant midday volatility as investors digested mixed news across software, cloud computing, and space technology segments. Oracle shares retreated 7%, surrendering a portion of Thursday’s gains despite confirming a major cloud computing partnership with Meta. This pullback occurred even as the company strengthens its position in the competitive cloud infrastructure market, where enhanced AI supervision tools are becoming increasingly crucial for enterprise clients.

Meanwhile, AST SpaceMobile faced a 6% decline following its spectacular recent performance, with Barclays delivering a double downgrade to underweight. The satellite communications company’s volatility highlights the unpredictable nature of emerging space technology investments. In contrast, Intuitive Machines gained 3% after Deutsche Bank upgraded the stock to buy, citing an attractive risk-reward profile and upcoming commercial catalysts in the computational modeling space that could drive future growth.

Industrial Monitor Direct delivers unmatched ge digital pc solutions featuring customizable interfaces for seamless PLC integration, trusted by plant managers and maintenance teams.

Pharmaceutical Stocks React to Political Pressure

The healthcare sector witnessed notable movement as obesity drug manufacturers Novo Nordisk and Eli Lilly both declined 3-4% following political commentary about potential price reductions. President Trump’s suggestion that obesity medication costs could be “much lower” created uncertainty in the pharmaceutical space, though CMS administrator Dr. Mehmet Oz clarified that White House negotiations hadn’t yet occurred. This development comes amid broader global governance discussions surrounding healthcare technology and pricing.

Revolution Medicines provided a bright spot in the sector, jumping 10% after receiving an FDA voucher for its multi-selective inhibitor daraxonrasib through the National Priority Voucher program. The treatment targets metastatic pancreatic ductal adenocarcinoma and metastatic non-small cell lung cancer, representing significant innovation in oncology therapeutics that could transform patient outcomes in these challenging disease areas.

Financial Institutions Show Mixed Results

Regional banks staged a modest recovery after Thursday’s sell-off, with the SPDR S&P Regional Banking ETF (KRE) advancing 1%. Zions Bancorporation led the group with a 4% rally following a Baird upgrade, while Western Alliance added 2%. This rebound demonstrates the sector’s sensitivity to analyst sentiment and broader global economic policy developments that influence interest rate expectations.

Investment bank Jefferies bounced back with a 4.2% gain after Thursday’s steep decline, boosted by an Oppenheimer upgrade to outperform. The firm reassured investors that Jefferies’ exposure to First Brands remains “very limited,” alleviating concerns about potential contagion risk. Meanwhile, Interactive Brokers Group fell 3% despite reporting better-than-expected third-quarter results, highlighting how even strong performance can sometimes disappoint elevated investor expectations in the current business leadership environment.

Infrastructure and Industrial Stocks Face Headwinds

Transportation and infrastructure companies displayed varied performance, with CSX climbing 3% on better-than-expected earnings. The railroad operator reported adjusted earnings of 44 cents per share on $3.59 billion in revenue, exceeding analyst projections. However, Core Scientific declined more than 5% after CoreWeave responded to investor opposition regarding its acquisition offer, calling its bid “best and final” in a move that could signal consolidation in quantum computing infrastructure.

Micron Technology faced a 2% decline following reports that the company will exit the server chips business in China, where its operations have struggled to recover from a 2023 ban on its products in critical infrastructure. This development reflects the ongoing challenges in navigating international technology markets amid evolving regulatory landscapes and geopolitical tensions.

For investors seeking to understand these complex market movements, comprehensive analysis of midday market movers provides valuable context for making informed decisions in this volatile trading environment.

Earnings Season Drives Individual Stock Performance

The ongoing earnings season continued to create significant single-stock volatility, with several companies moving sharply on their quarterly results. American Express surged 6% after beating expectations and raising full-year guidance, while Truist Financial gained 3.5% on stronger-than-anticipated results. Conversely, Bank OZK slipped 3% as its earnings missed expectations, and State Street declined more than 3% despite mixed results that included both earnings and revenue beats.

Fifth Third Bancorp posted a modest 1% gain following its better-than-expected earnings report, providing some stability after last week’s announcement of its Comerica acquisition. The diversified performance across financial institutions underscores the importance of fundamental analysis during earnings season, as company-specific factors often outweigh broader sector trends in driving short-term price action.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.